Understanding NYC state income tax is essential for anyone living or working in the bustling city. Whether you're a resident, a business owner, or someone who earns income within New York City, navigating the intricacies of state and local taxation can be daunting. With a combination of state and city taxes, residents face a higher tax burden compared to other regions. This guide aims to demystify the process, ensuring you're well-prepared for tax season and beyond.

As tax laws evolve and economic conditions shift, staying informed about NYC state income tax rates and regulations becomes crucial. This article will walk you through the key aspects of taxation in New York City, including brackets, exemptions, deductions, and credits. By the end, you'll have a clearer understanding of how these taxes impact your finances and how to optimize your tax strategy.

Whether you're filing for the first time or looking to refine your approach, this resource provides actionable insights and practical tips. From understanding how NYC state income tax applies to different income levels to exploring potential deductions, we'll cover everything you need to know. Let's dive in and unravel the complexities of New York's tax system.

Read also:Ashton Sanders A Rising Star In Hollywood

What Are the Current NYC State Income Tax Rates?

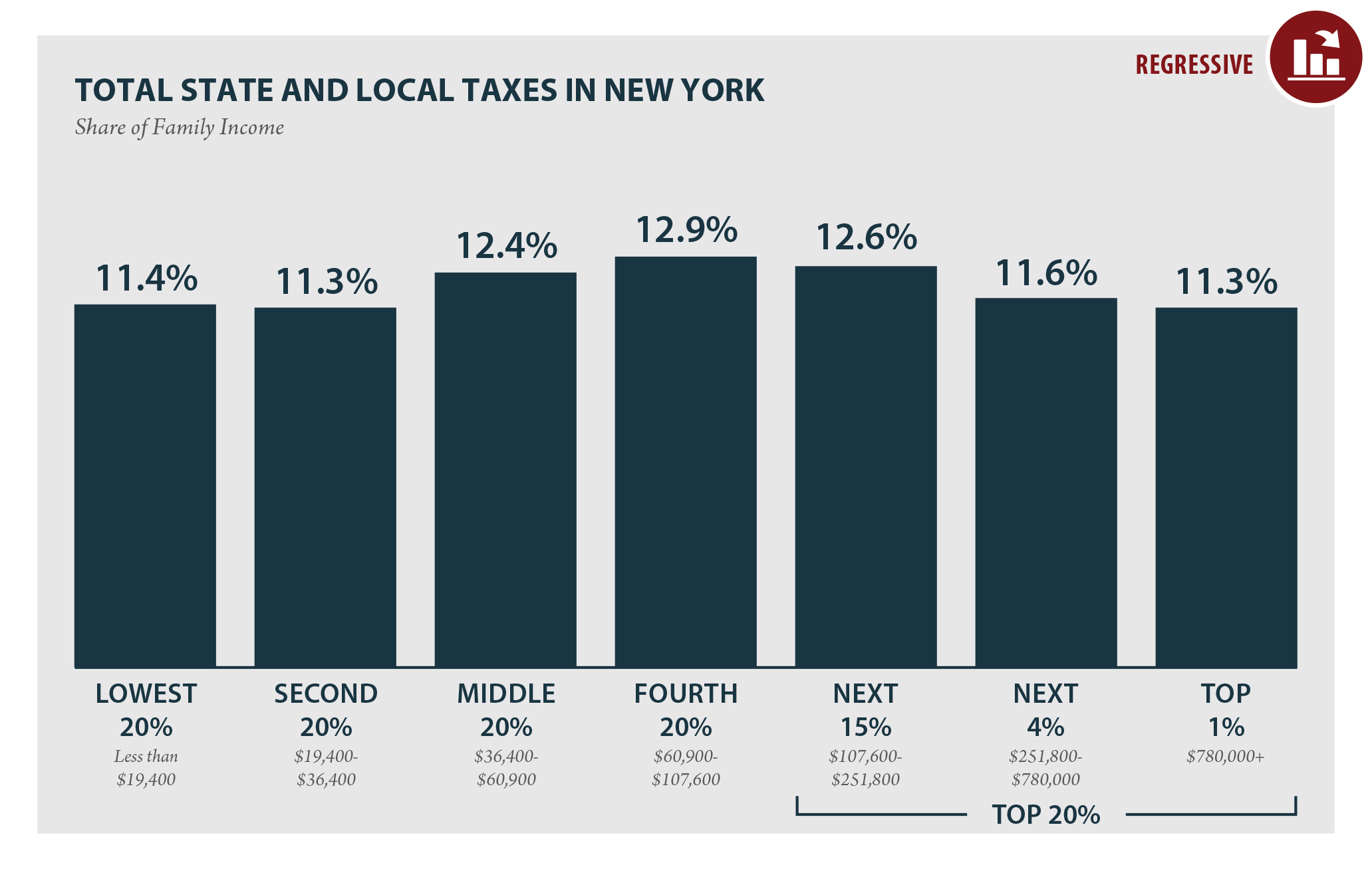

Tax rates in New York City are structured based on progressive brackets, meaning higher income levels are taxed at a higher percentage. The state income tax rates for New York are determined by the New York State Department of Taxation and Finance. For the 2023 tax year, the state rates range from 4% for lower income brackets to 8.82% for higher brackets. However, New York City imposes an additional city income tax, which varies depending on your filing status and income level.

Here’s a breakdown of the combined state and city tax brackets:

- Single filers earning up to $8,500 pay 4.458% in state tax and 2.907% in city tax.

- For those earning between $8,501 and $11,700, the state rate increases to 4.9%, while the city rate remains the same.

- Higher earners, with incomes over $21,550, face a combined rate that exceeds 12%, depending on their exact income level.

It's important to note that these rates are subject to change annually, so staying updated is critical for accurate tax planning.

How Does NYC State Income Tax Affect Residents?

Residents of New York City face a unique tax landscape due to the dual state and city income tax structure. This dual system means that residents pay both New York State taxes and New York City taxes. For instance, a single filer earning $50,000 annually would pay approximately $2,400 in state taxes and an additional $1,200 in city taxes, assuming standard deductions and exemptions are applied.

For families and individuals with higher incomes, the impact becomes even more significant. The cumulative effect of state and city taxes can significantly reduce take-home pay, making financial planning essential. Additionally, certain deductions, such as mortgage interest and charitable contributions, can help mitigate the tax burden, but they require careful documentation and planning.

Can Non-Residents Be Subject to NYC State Income Tax?

Yes, non-residents who earn income in New York City are also subject to NYC state income tax. If you work in the city but live elsewhere, you may still owe city income taxes on the income earned within the city limits. The rules for non-residents differ slightly from those for residents, primarily in terms of exemptions and deductions.

Read also:Juaacuterez Vs Santos The Ultimate Rivalry In Mexican Football

Non-residents typically pay a lower city tax rate compared to residents. However, they are still required to file a city income tax return if their income exceeds a certain threshold. It's important for non-residents to keep detailed records of their income sources to ensure compliance with both state and city tax requirements.

Who Sets the NYC State Income Tax Rates?

The New York State Department of Taxation and Finance is responsible for setting state income tax rates, while the New York City Department of Finance oversees city income tax rates. Both entities collaborate to ensure a cohesive tax system that aligns with state and local budgets. Tax rates are reviewed periodically and adjusted based on economic conditions, legislative changes, and budgetary needs.

Citizens and businesses often advocate for tax reform, especially in light of the city's high tax burden. Policymakers consider these inputs when proposing adjustments to tax brackets and rates. Understanding the governing bodies behind NYC state income tax helps taxpayers stay informed about potential changes and advocate for fair taxation.

What Deductions Can Help Lower NYC State Income Tax?

Several deductions can help reduce your NYC state income tax liability. Standard deductions are available for both single filers and married couples filing jointly. Itemized deductions, such as mortgage interest, property taxes, and charitable contributions, can further lower your taxable income. Additionally, education expenses, medical expenses exceeding a certain percentage of income, and business-related expenses may qualify for deductions.

For example, if you own a home in New York City, you can deduct mortgage interest payments up to a certain limit. Similarly, contributions to qualified retirement plans, such as 401(k)s or IRAs, can provide tax benefits. Keeping meticulous records of all eligible expenses is key to maximizing deductions and minimizing your tax burden.

Is There a Cap on NYC State Income Tax Deductions?

Yes, there are caps on certain deductions under NYC state income tax regulations. For instance, the mortgage interest deduction is limited to interest paid on up to $750,000 of qualified residence loans. Charitable contributions are deductible up to 60% of your adjusted gross income (AGI). Understanding these limits is crucial to ensure compliance and avoid potential penalties.

Furthermore, phase-out rules may apply to itemized deductions for higher-income taxpayers. These rules gradually reduce the amount of deductions available as income increases, adding another layer of complexity to tax planning. Consulting a tax professional or utilizing tax preparation software can help navigate these nuances effectively.

How Can You File for NYC State Income Tax?

Filing NYC state income tax involves completing both state and city tax returns. The New York State Department of Taxation and Finance provides forms IT-201 for state taxes and IT-2105 for city taxes. These forms are available online or through certified tax preparers. E-filing is encouraged, as it reduces processing times and minimizes errors.

When filing, ensure you have all necessary documents, including W-2 forms, 1099 forms for freelance income, and receipts for deductible expenses. Double-check all calculations and entries to avoid costly mistakes. Filing deadlines typically align with federal tax deadlines, so mark April 15th on your calendar to ensure timely submission.

Why Is NYC State Income Tax Higher Than Other States?

NYC state income tax rates are higher than in many other states due to the city's high cost of living and extensive public services. Funding for infrastructure, education, public safety, and social services contributes to the need for higher tax revenues. Additionally, New York City's role as a global financial hub attracts a concentration of high-income earners, justifying a progressive tax structure.

Comparing NYC state income tax rates to other states highlights the disparity. For example, states like Florida and Texas have no state income tax, while others, such as California, impose similar or slightly higher rates. However, the combination of state and city taxes in New York City makes the overall tax burden one of the highest in the nation.

What Are the Consequences of Not Paying NYC State Income Tax?

Failing to pay NYC state income tax can result in severe consequences, including penalties, interest charges, and legal action. The New York State Department of Taxation and Finance imposes penalties for late filing and late payment, which can accumulate over time. In extreme cases, unpaid taxes may lead to wage garnishment, asset seizures, or even criminal charges.

To avoid these repercussions, it's vital to file your taxes on time and pay any owed amounts promptly. If you're unable to pay the full amount, consider setting up a payment plan with the tax authorities. Demonstrating good faith efforts to resolve tax obligations can help mitigate penalties and maintain financial stability.

Table of Contents

- What Are the Current NYC State Income Tax Rates?

- How Does NYC State Income Tax Affect Residents?

- Can Non-Residents Be Subject to NYC State Income Tax?

- Who Sets the NYC State Income Tax Rates?

- What Deductions Can Help Lower NYC State Income Tax?

- Is There a Cap on NYC State Income Tax Deductions?

- How Can You File for NYC State Income Tax?

- Why Is NYC State Income Tax Higher Than Other States?

- What Are the Consequences of Not Paying NYC State Income Tax?

In conclusion, navigating NYC state income tax requires a comprehensive understanding of the tax system, rates, deductions, and filing procedures. By staying informed and proactive, you can effectively manage your tax obligations and optimize your financial well-being. This guide serves as a valuable resource to help you navigate the complexities of New York City's tax landscape with confidence.

![NYC & NYS Tax Calculator [Interactive] Hauseit](https://www.hauseit.com/wp-content/uploads/2023/02/NYC-Income-Tax-Calculator.jpg)