When it comes to managing finances, understanding NYC state tax is crucial for residents and businesses alike. New York City operates with a unique tax structure that combines state and local taxes, making it essential for individuals to stay informed about their obligations and benefits. Whether you're a new resident or a long-term New Yorker, navigating the complexities of NYC state tax can be overwhelming. This guide aims to provide clarity on the intricacies of taxation in the city, offering actionable insights to help you make informed decisions.

As one of the most populous and economically vibrant cities in the United States, New York City imposes a variety of taxes that contribute to its infrastructure, public services, and social programs. Residents are subject to both state and city-level taxes, creating a layered system that requires careful planning and understanding. In this article, we'll delve into the nuances of NYC state tax, breaking down key components, offering tips for compliance, and highlighting potential savings opportunities.

With ever-changing regulations and updates, staying up-to-date on NYC state tax laws is vital for financial stability. From income tax to sales tax, this article will equip you with the knowledge necessary to navigate the tax landscape effectively. By the end of this guide, you'll have a comprehensive understanding of your tax obligations and how to optimize your financial strategy.

Read also:Felix Augeraliassime The Rising Star Of Tennis

What Are the Key Components of NYC State Tax?

NYC state tax encompasses several components, each playing a significant role in the city's revenue generation. The primary taxes include income tax, sales tax, property tax, and business tax. Understanding these components is the first step toward effective financial planning. Let's explore each in detail:

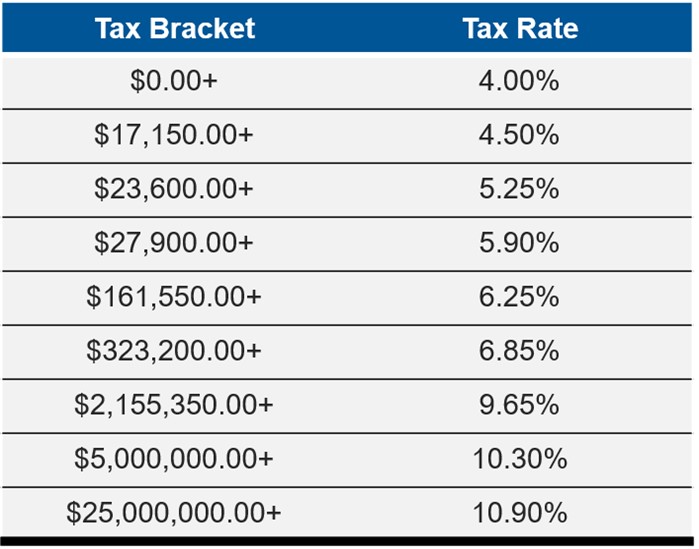

- Income Tax: Both New York State and New York City impose income taxes on residents. The rates vary depending on income levels, with higher earners paying a larger percentage.

- Sales Tax: Residents and visitors are subject to a combined state and local sales tax rate of approximately 8.875% in most areas of NYC.

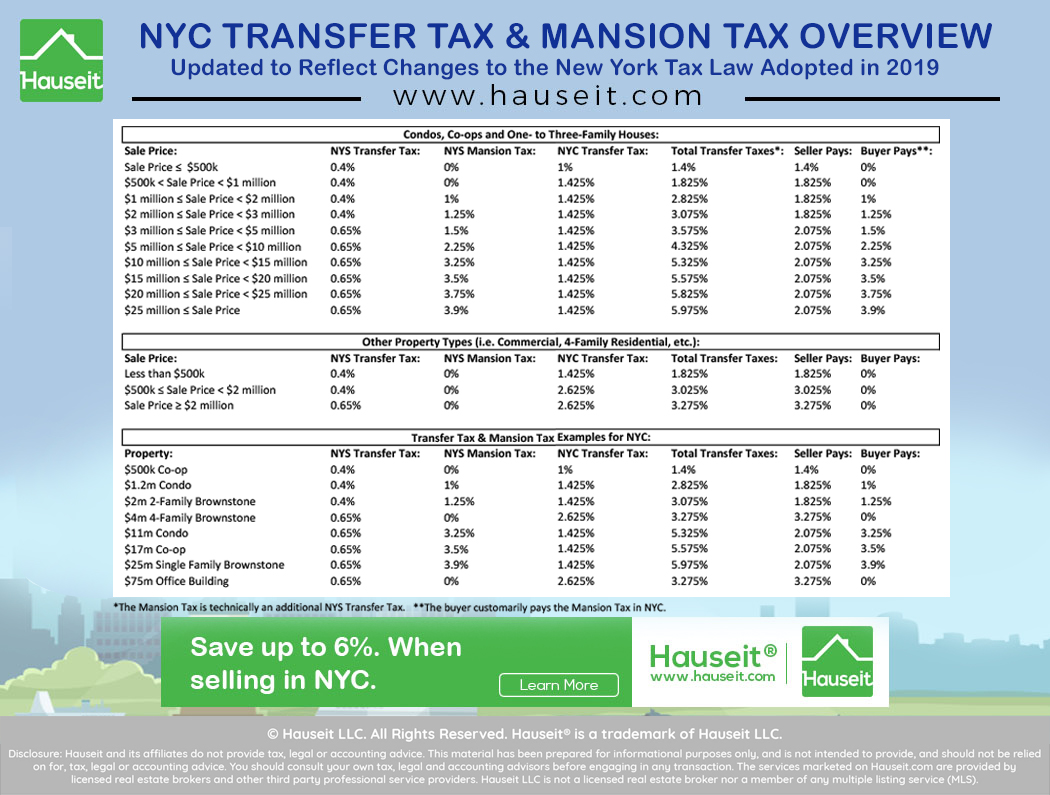

- Property Tax: Property owners in NYC pay taxes based on assessed values, with rates differing across the five boroughs.

- Business Tax: Businesses operating in NYC must comply with various tax obligations, including corporate income tax and unincorporated business tax.

How Does NYC State Tax Impact Residents?

The impact of NYC state tax on residents varies depending on individual circumstances. For instance, homeowners may face higher property tax burdens compared to renters. Similarly, high-income earners might experience a more significant portion of their income being taxed. Understanding these impacts can help residents strategize effectively:

For example, individuals earning above a certain threshold may benefit from exploring tax deductions and credits to reduce their overall liability. Additionally, staying informed about changes in tax laws can help residents take advantage of new opportunities for savings. The complexity of NYC state tax necessitates a proactive approach to financial management.

Can You Avoid Common Pitfalls in NYC State Tax?

Avoiding common pitfalls in NYC state tax requires awareness and preparation. Many residents encounter issues such as underpayment, late filing, or failure to claim eligible deductions. To prevent these mistakes, consider the following tips:

- File your tax returns on time to avoid penalties.

- Keep detailed records of all income and expenses throughout the year.

- Consult with a tax professional for personalized advice tailored to your situation.

Why Is Understanding NYC State Tax Important for Businesses?

Businesses operating in NYC face unique challenges when it comes to taxation. From corporate income tax to unincorporated business tax, understanding NYC state tax is crucial for maintaining compliance and optimizing profitability. Businesses must navigate a complex regulatory environment, ensuring they meet all obligations while minimizing their tax burden.

For example, small business owners may benefit from exploring available tax credits and incentives designed to support entrepreneurship in NYC. Larger corporations, on the other hand, might focus on strategic tax planning to maximize deductions and reduce liabilities. Regardless of size, staying informed about NYC state tax regulations is essential for long-term success.

Read also:Investing In Walmart Stock A Comprehensive Guide For Investors

What Are the Common Misconceptions About NYC State Tax?

Misconceptions about NYC state tax can lead to costly mistakes and missed opportunities. One common myth is that residents only need to worry about state-level taxes, ignoring the additional city-level obligations. Another misconception is that all deductions and credits are universally applicable, leading some individuals to overlook valuable opportunities for savings.

By addressing these misconceptions, residents and businesses can make more informed decisions about their financial strategies. For example, understanding the differences between state and city tax rates can help individuals plan for their obligations more effectively. Additionally, recognizing the availability of specific deductions and credits can lead to significant savings.

How Can Residents Reduce Their NYC State Tax Liability?

Reducing NYC state tax liability involves a combination of strategic planning and proactive measures. Residents can take advantage of various deductions, credits, and exemptions to lower their overall tax burden. Some effective strategies include:

- Claiming the New York State Earned Income Tax Credit (EITC) if eligible.

- Utilizing property tax exemptions for homeowners, such as the Senior Citizen Exemption.

- Maximizing contributions to retirement accounts, which can reduce taxable income.

Additionally, staying informed about changes in tax laws can help residents identify new opportunities for savings. For example, recent updates to NYC state tax regulations may introduce new deductions or credits that were not previously available.

What Role Does NYC State Tax Play in City Development?

NYC state tax plays a critical role in funding the city's infrastructure, public services, and social programs. The revenue generated from various taxes supports essential initiatives such as transportation, education, healthcare, and public safety. Understanding the connection between taxation and city development can help residents appreciate the importance of fulfilling their tax obligations.

For instance, the funds collected through NYC state tax contribute to the maintenance and improvement of subway systems, schools, and hospitals. By paying their fair share, residents and businesses help ensure the continued growth and prosperity of the city. This interconnectedness highlights the significance of responsible tax management for all stakeholders.

Is It Necessary to Hire a Tax Professional for NYC State Tax?

Hiring a tax professional can be beneficial for individuals and businesses navigating the complexities of NYC state tax. Tax professionals possess specialized knowledge and expertise, enabling them to provide tailored advice and guidance. While not mandatory, engaging a professional can help ensure compliance, optimize savings, and avoid potential pitfalls.

For example, a tax professional can assist with identifying eligible deductions and credits, preparing accurate tax returns, and addressing any issues that may arise during audits. Additionally, they can stay updated on changes in tax laws, ensuring their clients remain informed and compliant. The decision to hire a professional ultimately depends on individual needs and circumstances.

NYC State Tax and the Future: What Can Residents Expect?

The future of NYC state tax is shaped by ongoing legislative changes and economic developments. As the city continues to grow and evolve, residents can expect adjustments to tax rates, regulations, and incentives. Staying informed about these changes is crucial for adapting financial strategies accordingly.

For example, recent proposals to increase income tax rates for high earners or introduce new business taxes highlight the dynamic nature of NYC state tax. Residents and businesses must remain vigilant, ensuring they understand the implications of these changes and adjust their plans as necessary. By maintaining awareness and flexibility, individuals can navigate the evolving tax landscape with confidence.

Conclusion: Mastering NYC State Tax for Financial Success

In conclusion, mastering NYC state tax is essential for achieving financial success in the city. By understanding the key components, impacts, and strategies for compliance, residents and businesses can optimize their financial strategies and reduce their tax liabilities. Staying informed about changes in tax laws and regulations is crucial for adapting to the evolving landscape.

Whether you're a homeowner, small business owner, or high-income earner, taking a proactive approach to NYC state tax management can lead to significant benefits. By leveraging available deductions, credits, and exemptions, you can minimize your obligations while maximizing your savings. Remember, the key to success lies in knowledge, preparation, and professional guidance when needed.

Table of Contents

- Understanding NYC State Tax: A Comprehensive Guide for Residents

- What Are the Key Components of NYC State Tax?

- How Does NYC State Tax Impact Residents?

- Can You Avoid Common Pitfalls in NYC State Tax?

- Why Is Understanding NYC State Tax Important for Businesses?

- What Are the Common Misconceptions About NYC State Tax?

- How Can Residents Reduce Their NYC State Tax Liability?

- What Role Does NYC State Tax Play in City Development?

- Is It Necessary to Hire a Tax Professional for NYC State Tax?

- NYC State Tax and the Future: What Can Residents Expect?